Before you start touring homes, it helps to answer one big question: how much house can you actually afford? Setting a realistic budget early keeps your search focused and your finances comfortable long after you move in.

It is easy to fall in love with a home that stretches your budget, but the goal is a payment you can live with happily for years. Whether you are a first-time buyer exploring FHA loans Dallas TX programs, a current homeowner considering a Texas home refinance, or comparing home equity loans in Texas to unlock your next move, knowing your range before you shop helps you avoid disappointment and make confident decisions.

Here is how affordability really works in Texas, the factors that shape your budget, and how to estimate a price range you can feel good about.

Affordability Is About More Than the Sticker Price

The price of a home is only part of the story. What you can afford depends on the full monthly cost of owning, including property taxes and insurance, and how that fits alongside the rest of your budget.

In Texas, property taxes are a meaningful part of that picture, so they deserve attention from the very beginning. Two homes with the same price can carry different monthly costs depending on their tax and insurance picture, which is why looking at the whole payment matters. Experienced home lenders Texas buyers trust can help you see the full cost before you commit.

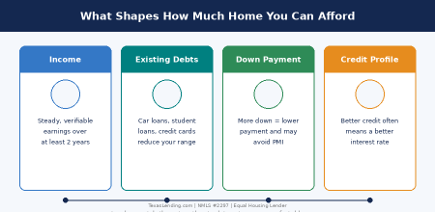

The Main Factors Lenders Consider

When a lender looks at how much you can borrow, they weigh several things together rather than focusing on any single number:

- Your income and how steady and reliable it is.

- Your existing monthly debts, from car loans to credit cards.

- Your down payment and overall savings.

- Your credit profile and payment history.

A helpful concept here is your debt-to-income ratio, which compares your monthly debt payments to your monthly income. Lenders use it to gauge how much of a new mortgage payment fits comfortably into your budget. The lower your existing debt, the more room you generally have.

📖 Related: Low Down Payment Mortgage Options — Explore purchase programs that require as little as 3% down.

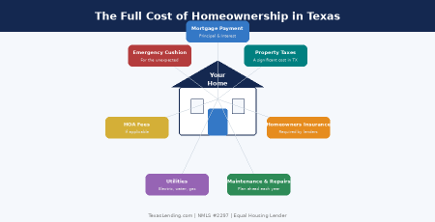

Do Not Forget the Full Cost of Ownership

A home you can technically qualify for is not always a home that fits your life. Beyond the mortgage payment, it is wise to plan for:

- Property taxes and homeowners insurance. Texas property tax rates vary by county and can significantly affect your monthly payment.

- Routine maintenance and the occasional repair. Budget for upkeep costs each year.

- Utilities and any community or HOA fees. These ongoing costs add up and affect your monthly cash flow.

- An emergency cushion for the unexpected. Having reserves protects you when surprises come up.

Leaving room for these costs helps you avoid stretching too thin once you own the home. A comfortable budget is one that still works on a tight month, not just an easy one. Homeowners exploring home equity in Texas to fund renovations or consolidate debt should factor these carrying costs into their plan as well.

📖 Related: Custom Down Payment Savings Plan — Build a personalized timeline to reach your down payment goal.

Estimate Your Range with a Calculator

A Mortgage Calculator Texas homebuyers can access right here at TexasLending.com is a quick way to turn these factors into a working estimate. By adjusting the home price, down payment, and loan term, you can see how the monthly payment shifts and find a range that feels sustainable.

Use it as a starting point to explore different scenarios — whether you are comparing purchase options, reviewing Texas home refinance rates, or looking at Dallas refinance rates for an existing mortgage. A calculator gives you a helpful ballpark; a lender gives you a personalized answer.

→ Use Our Purchase Calculator ←

Get a Personalized Answer with Pre-Approval

Calculators are great for rough figures, but a pre-approval gives you a clearer, personalized number. A lender reviews your income, debts, and credit to tell you what you can realistically borrow. It also makes your offer stronger when you find the right home, since sellers know your financing is in order.

Think of pre-approval as turning a guess into a plan. With a clear number in hand, you can shop with confidence and move quickly when the right home appears. At Texaslending, our licensed mortgage consultants can walk you through the process and help you explore competitive Texaslending rates across conventional, FHA, and VA programs.

→ Get Pre-Approved Free with TexasLending.com ←

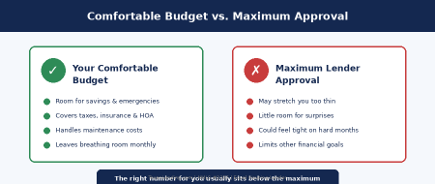

The Comfortable Budget Versus the Maximum

One of the most useful distinctions in home buying is the gap between what a lender will approve and what actually fits your life. A pre-approval tells you the ceiling, but the right number for you usually sits below it. Leaving room in your monthly budget means you can absorb surprises, keep saving, and still enjoy the home you buy rather than feeling stretched by it.

A helpful exercise is to picture your target monthly payment alongside everything else you spend in a typical month. If that payment leaves comfortable breathing room, you are likely in a sustainable range — even if a lender would let you go higher.

How Your Down Payment Changes the Picture

Your down payment does more than reduce the amount you borrow. A larger down payment can lower your monthly payment and may help you avoid private mortgage insurance on a conventional loan, while a smaller one can help you buy sooner. There is no single right answer; it depends on your savings, your timeline, and how the monthly numbers feel. Running a few scenarios with different down payment amounts is one of the clearest ways to see what works best for you.

Current homeowners interested in Texas home equity lending options may also be able to use existing equity toward a down payment on a new property, or to consolidate higher-rate debt through a cash-out refinance Houston homeowners have found effective for strengthening their overall financial position.

Ultimately, the most reliable way to know what you can afford in Texas is to combine a quick calculator estimate with a conversation about your full financial picture. A calculator gives you a starting range in minutes, and a lender can refine it based on your income, debts, and goals so you can shop with confidence.

📖 Related: Home Equity Loans in Texas — Learn how Texas home equity lending works and whether it fits your plan.